Frequently Asked Questions

- Click question to view answer.

- Search all categories or a specific category selected from the list at right.

Encumbrances

You can use the Workday report “Find Purchase Orders” to find open POs. Make sure to update the "Document Date On or After" field to 7/1/2023 to bring in the right population.

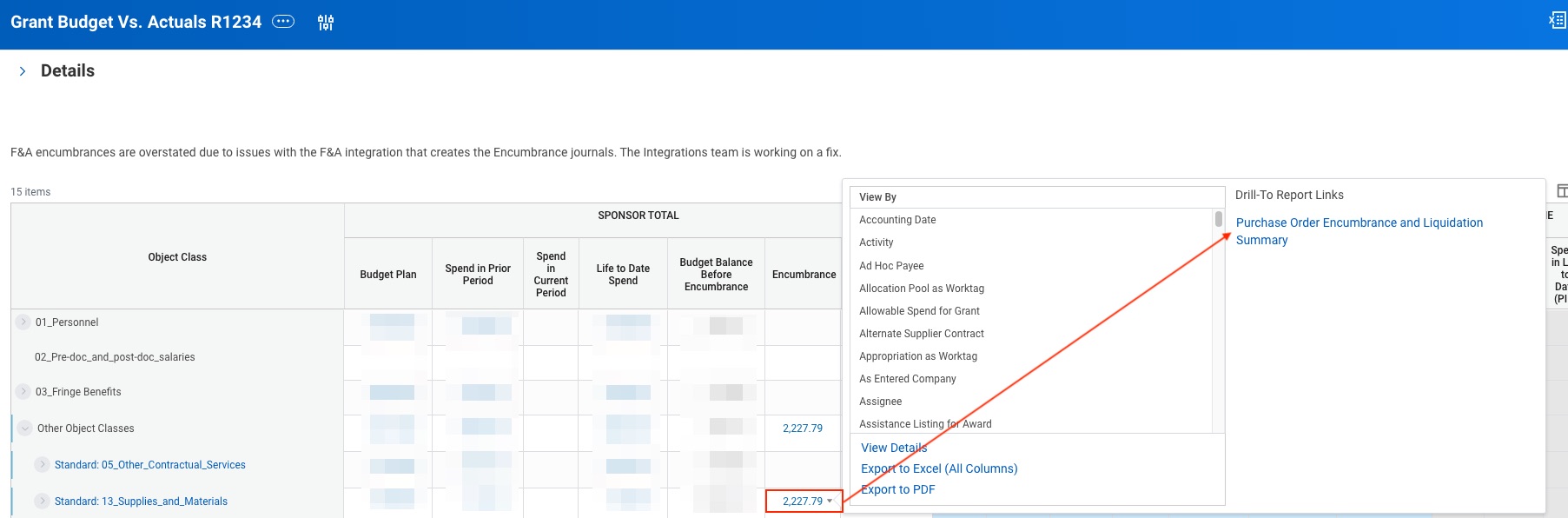

You can also use the Workday report "Grant Budget Vs. Actuals R1234". It displays encumbrances and pre-encumbrances by default. Click on the grey triangle next to encumbrance and pre-encumbrance amounts to reveal a drill-down report. This may provide additional information about the purchase order, requisition, spend authorization et al.

Expenditures

Expenditures displayed on Transaction Summary reports in MyFD (MyFinancial.desktop) come from various sources. Often the source can be identified by the description or reference information in the Transaction Summary. If you need to locate a copy of the source document, here are some resources that may assist you:

- For payroll charges, contact the Integrated Service Center at: ischelp@uw.edu or 206.543.8000.

- For Purchase Orders, contact Procurement Customer Service at: pcshelp@uw.edu or 206.543.4500.

- For questionable ISDs (Internal Sales Document), CTIs (Cost Transfer Invoice), or CTs (Cash Transmittal), review the information in the reference fields for contact information, or use the Originating Area Code found in the Transaction Detail of an expenditure or revenue entry to find out who processed it.

- JVs (Journal Vouchers) can be processed by multiple areas. The characters after the identifier of "JV" denote which area processed the document. To determine which department to contact with JV questions, contact Financial Accounting.

Grant Tracker

Grant Tracker is a website accessing a database containing information on all GCA budgets. It is designed to reduce the amount of time to close budgets, provide information in a timely manner, and decrease the number of requests for information to and from GCA.

Features include:

- View all GCA budgets

- Access parent and sub budget information

- View invoices and reports

- Submit requests and attachments to GCA

- Get up-to-date status on outstanding requests

- View request/attachment history

- Submit Transpasu requests for new sub budgets

- Transfer deficit balances

- Provide up-to-date campus contacts to receive GCA messages

Invoicing

Normally GCA (Grant and Contract Accounting) initiates and mails invoices for grants and contracts that require billing.

At times, however, GCA needs department input to complete invoicing:

If a budget is set up for milestone invoicing, GCA relies on the department to inform us that a deliverable has been completed and an invoice can be issued.

Some sponsors require detailed backup that GCA has no access to (e.g. receipts, timesheets, or activity reports). In these cases GCA will prepare the invoice and then route it to the department via Grant Tracker to provide the needed backup and route to the sponsor.

For clinical trial budgets, the department is responsible for invoicing.

Invoices are linked from a budget's Grant Tracker Budget Information page. Click on the invoice number hyperlink to download a PDF copy.

Two caveats:

- If a sponsor has a unique invoice template rather than one of our standard formats, the actual invoice sent to the sponsor will not match our internal invoice as shown on Grant Tracker.

- Grant Tracker updates overnight, so invoices will appear the day after they are issued in our invoicing system.

If the sponsor contacts the department for backup detail on a particular invoice (e.g. receipt copies for travel or equipment expenditures), the department may respond to them directly. Otherwise, please forward the communication to gcahelp@uw.edu.

GCA cannot issue invoices on a budget in advance status because we do not yet have a fully executed agreement between UW and the sponsor confirming the terms of the agreement. However, in rare cases we can make an exception if the sponsor themselves request it, e.g. so they can pay the award or a portion thereof in advance or if they need to complete payment during an expiring fiscal period. In these cases, please contact GCA via Grant Tracker or email to gcahelp@uw.edu.

If a sponsor hasn't received the invoice within a week of its issuance, we may not have the correct mailing or email address on file for them. If a sponsor expresses concern over not having received an invoice, please forward their message to gcahelp@uw.edu and we will follow up with them.

When there is a question regarding a payment made to a grant/contract budget, email gcahelp@uw.edu or submit a question using Grant Tracker (will open a new window).

The remittance address for check payments for a grant or contract is:

University of Washington

Grant and Contract Accounting

12455 Collections Drive

Chicago, IL 60693-0001

If a department receives a payment for a grant or contract budget, please send it to the Chicago remittance address. Be sure to write the Workday grant worktag number (GR######) near the memo line of the check and forward a PDF copy of all supporting documentation to gcacash@uw.edu.

Please ensure that your check is made payable to "University of Washington," and send payments via standard postal mail only. (The lockbox facility is not set up to receive documents from other delivery services, and such payments may be delayed or lost.)

Payment information for invoices issued by GCA is available on the award's Budget Information page on the Grant Tracker website. Any unpaid amount will be listed in the "Open" column in the Financial Information section. The Invoices section lists all invoices issued by amount, with any open amount for each, and the Payments section provides details on individual payments, including which invoices they were applied to and the date payments posted.

Note that grant and contract invoice payments are NOT reflected in MyFinancial.desktop (MyFD). The MyFD Budgeted and Revenue amounts are based on the funding the sponsor has committed to the award, regardless of whether payment has been received yet or not.

To ensure checks are applied to sponsored project activity in a timely manner while we are working remotely, please send checks directly to our lockbox:

University of Washington

Grant and Contract Accounting

12455 Collections Drive

Chicago, IL 60693-0001

Be sure to write the budget number near the memo line on the check and forward all supporting documentation to gcacash@uw.edu. We plan to resume normal operations (GCA campus mailbox 354966 or hand delivery) once the University’s recommendation to telework is lifted.

Invoices generated by GCA’s invoicing software are automatically updated to a budget’s Grant Tracker Budget Information page the day after they are created. If you do not see an invoice you are expecting, please send a Grant Tracker question under the Invoicing topic.

Check the budget information page in Grant Tracker. In the Financial Information section, the last three items, Invoice, Receipt and Open, reflect the cumulative amount invoiced, the total payments received from the sponsor, and the amount remaining unpaid. Also, you may check if a specific invoice has been paid by scrolling down to the Invoices section and checking the Open Amount column.

Please forward the request to gcahelp@uw.edu so that we can provide the information and sign off on any forms the sponsor requires.

GCA cannot accept credit card payments. Sponsors may pay by check (including cashier’s check) or wire/ACH.

By default charges to parent and sub-budget(s) are combined on a single invoice. However, if a sponsor requests separate invoicing for a sub-budget, please notify GCA via a Grant Tracker in the Invoicing topic, and we can accommodate their request.

Notify GCA by Grant Tracker in the Invoicing topic or by forwarding the sponsor’s email to gcahelp@uw.edu. We will follow up with them to locate the payment.

Note that GCA does not issue a final invoice until the Final Action Date has passed. Departments are required to ensure that all expenditures have posted by then, and if that is impossible to notify GCA of the pending charges on or before that date. However, if there are additional charges the department was unaware of at the Final Action Date and the sponsor provides written confirmation they will accept a revised final invoice, GCA will invoice the additional charges. Please submit a Pending Transactions Detail Form via Grant Tracker along with your sponsor confirmation to request a supplemental invoice.

When a sponsor discovers an unallowable expense, it is the department’s responsibility to transfer it off their budget as soon as possible. The transfer will result in a credit on the next invoice issued. Because of this, we discourage sponsors from short-paying invoices. Instead, we prefer to void the invoice with the unallowable charge and issue a replacement after the charge has been removed.

Here are the steps to see payment information in Workday:

- Open your award in Workday

- Go to the Billing & Receivables tab

- Go to the View Sponsor Invoices for Award sub-tab

- You'll see a table that includes a list of invoices and the Payment Status for each invoice.

- If an invoice's Payment Status is Paid, you can click on the invoice you're interested in.

-

In the View Customer Invoice window, click on the Activity tab toward the bottom of the screen.

From here you can either:

View the accounting journal associated with the payment (click on the magnifying glass in the Transaction column) or

View additional information about the payment itself (click on Payment hyperlink)

Journal Vouchers

What is a Journal Voucher (JV)?

Journal Vouchers (also known as JVs) are forms used to process accounting entries. They are primarily used for fund transfers and corrections. Many central offices process JVs.

For more information on which office to contact about a JV, contact Financial Reporting.

Organization Codes

To change an individual budget's org code, please send a Grant Tracker request under the Budget Setup topic. If you need to change the org codes for multiple budgets at once, please prepare a list or spreadsheet of the changes required and email it to gcahelp@uw.edu.

Parent/Sub

RRF budgets are granted through the University’s Office of Research, and are to be used in advancing research in new directions. The Office of Research approves all requests to close an RRF budget. They need to have received, for review, the PI’s final report, a final summary of expenditures, and a final BSR (Budget Status Report) for the RRF being closed. Once reviewed and approved, the Office of Research will send an email with official approval to close. This official email approval should be pasted into a Grant Tracker in the Closing topic.

For more information visit the Royalty Research Fund site.

Karen Luetjen, or Peter Wilsnack can be contacted for specific questions. Karen can be reached at: luetjen@uw.edu, or at 206.616.9089. Peter can be reached at: doogieh@uw.edu, or at 206.685.9316.

Residual Balance Transfers

In most cases, the answer is "no." However, the answer is "yes" if your award falls into one of the following categories:

- a clinical trial award

- a firm fixed price contract

- has written sponsor approval to keep the unspent the balance

Unspent balances from sponsored program awards must be transferred to a residual balance worktag. Please give GCA your residual balance worktag, and we will transfer the balance when we close the award line. If the surplus is greater than 25% of the award amount, you must confirm that all the work has been completed and provide a justification. (In rare cases, surpluses in budgets other than clinical trials or fixed price contracts may be retained, but only with explicit written authorization from the sponsor.)

If you need a new residual balance worktag, follow the process in the Worktag Template UW connect article.

Visit our Closing Your Award webpage for more information.