Miscellaneous Payments are a way of making a one-time payment to Non-UW employees that are US Citizens, Resident Aliens and Nonresident Aliens in Workday.

Important: If the payee is a foreign national or the payment relates to an international engagement, review Global Operations Support guidance and do the following:

- Carry out Restricted Party Screening

- Follow the International Activity Assessment Process (IAAP) when applicable

Please take these steps before submitting the Miscellaneous Payment in Workday:

- For general information about making payments to foreign nationals, visit the Making Payments to Foreign Nationals page on the Global Operations Support website.

- For restricted parties/sanctions and other research security considerations related to international engagements:

- Carry out Restricted Party Screening

- Follow the International Activity Assessment Process (IAAP) when applicable

In Workday:

- Review job aid How to Perform Miscellaneous Payments in Workday in UW Connect Finance Portal

- Security role needed: Miscellaneous Payment Data Entry Specialist

- Please refer to the job aid for a list of spend categories that are allowable and the tax status.

Helpful Reports in Workday:

- View Miscellaneous Payee

- Miscellaneous Payment Search R1372

Payment Types:

- Awards/Prizes

Used to pay awards and prizes for Non-UW Employees. Can be used for UW Students only if there is no stipulation on how funds are to be used by the student. Examples of this are awards or recognition for a special achievement, such as winning a judged competition, where the money can be used for any purpose. See Student Prizes and Awards

Recommended - When submitting the request, attach the award and/or prize letter.

- Honoraria

An honorarium is an amount of money paid to a professional person for which fees are not legally or traditionally required in recognition of a special service. The individual receiving the honorarium MAY NOT be an employee of the UW.

What qualifies as an honorarium?

- A lecture or talk

- A colloquium

- An address

- Grand Round

- A continuing education presentation or similar activity given to students, staff, faculty and/or the public at large

What does not qualify as an honorarium?

- Payments to companies or other institutions

- Personal Services or consulting services such as analyzing, design, planning, facilitating, interpretation, marketing, performing, programming or organization development, research or scientific studies, strategic planning, video production, organizational assessment, quality assurance, editing or reviewing.

Recommended - When submitting the request, attach documentation (i.e. letter of invite) justifying the honorarium

- Insurance

Insurance

- Non-Employee Travel Reimbursement

- Review the Travel website for guidance on travel policy

- To ensure a Miscellaneous Payee does not receive a 1099 for non-employee travel, fill out and attach the Non-Employee Travel Form.

- Non-UW Scholarships

Used to pay scholarships to Non-UW students or Non-UW employees, such as a department awarding a scholarship to a student attending a different school or paying a Non-UW individual for participating in a training or conference.

- Refund

This category should only be used on transactions that are pre-approved by the unit and AP.

- Reimbursement

Examples of reimbursable expenses include: conference fees, membership dues, non-travel related meals supplies, and supplies

What are not reimbursable expenses: personal services, UW tuition, housing, travel (see non-employee travel reimbursement category)

See other reimbursement information on the Reimbursements page

- Research Subject Payments

Research projects involving human subjects often offer a small payment to the research subjects for purposes of recruitment or encouragement for participation in the project.

- Royalties

A royalty is a payment to the legal owner of a property, patent or copyrighted work for the right to use the intellectual or physical assets owned by the licensor. Royalties do not include services.

What qualifies as a royalty payment?

- Copyright or patent payments

- Rights to use/license fees to photographers for use of their photo

- Permission fees

- Usage fees

- Service

Used to pay personal services (excluding Honoraria) such as consulting, design, analyzing, editing/reviewing, strategic planning, and teaching for non-UW courses under the Direct Buy Limit.

- Payment of personal services to individuals is subject to the Direct Buy Limit and current purchasing policies.

- Attach a copy of the individual's invoice.

- The spend category must be 1099 reportable. Please refer to the job aid for a list of spend categories that are allowable to use with Miscellaneous Payments.

- Services submitted as an MP should be used for one-time invoices. If an individual is expected to perform recurring services, they should register as a UW supplier and be paid through Supplier Invoice Request.

- Settlement

Settlement

- Stipend

A payment that is made to an individual to support a training or learning experience. For a payment to be considered a Stipend, certain criteria must be met.

Please note that the Stipend request category is a UW-specific payment definition and can only be used for Domestic payees. It cannot be used for payments to Foreign National Payees as "stipend" is not a payment type that is recognized by the IRS for tax reporting purposes. When making payments to Foreign National Payees, please review the Payments to Foreign Nationals Webpage for acceptable payment types.

Stipends are not considered wages if they are payment for a training or learning experience and not a payment for services rendered.

All Stipend requests must include documentation describing the proposed Stipend payment, describing the training program for which the Stipend is paid and sufficient to establish that the Stipend payment is a non-compensatory payment to defray living expenses during the period of a UW program.

UW Student Stipends should be paid through the Student Database (SDB) and will be reported at year end on a 1098-T tax form.

- UW employees' Stipends must be paid through UW Payroll

- See this ISC page for more information.

- Recommended - When submitting the request, attach documentation justifying the stipend.

- Workstudy/Grant

Intended for Student Fiscal Services (SFS)

What is Not Allowed

| Payment Type | Instead Use |

|---|---|

| Individuals who have an active Supplier number | Requisition or Supplier Invoice Request |

| Service payment over the Direct Buy Limit | Requisition |

| Payment for goods (i.e. artwork or equipment) | Requisition or Supplier Invoice Request |

| Payment to a company or business using an EIN | Requisition or Supplier Invoice Request |

| Current Employees (Exception: Royalties & NIH Childcare Allowance) | Payroll or Expense Report (Exception: Royalties and Contingent Worker, and NIH Childcare Allowance) More information: Independent Contractor Policy |

| Student Employees | Workday |

| Former Employees | Fill out the Form 1632 to determine the appropriate classification, and attach the completed form to the Miscellaneous Payment in Workday. |

Best Practices and Other Considerations

- Effective July 1, 2026: Changes to requirements for ACH payments on Miscellaneous Payments

Effective July 1, 2026, Banking and Accounting Operations (BAO) has implemented an updated ACH Risk Management & Compliance Policy in response to the 2026 rule updates from the National Automated Clearing House Association (NACHA), which require adoption of such a policy. See the full policy on the UW ACH Risk Management & Compliance Policy (Banking and Accounting Operations).

All University of Washington departments, auxiliary enterprises, and service centers that issue and receive ACH payments from/to the University of Washington are required to comply with this policy. As a result, changes to required attachments for MPs submitted using the “ACH” payment method will be implemented.

Additional Requirements for ACH Payments on Miscellaneous Payments

For all MPs submitted with the “ACH” payment type, departments will need to verify the following directly with the payee before submitting the payment request:

- Bank routing (ABA) number

- Bank account number

- Account type (checking or savings)

- Payee name as it appears on the bank account

The fraud prevention process for outgoing ACH payments applies only to transactions of $5,000 USD or greater ("ACH Transaction Threshold") involving new payees or any changes to existing payee banking information. BOA will review the ACH Transaction Threshold annually and may adjust it based on the effectiveness of the controls, emerging fraud trends, transaction activity, and other relevant risk factors.

What needs to be uploaded to Workday?

For ACH payments that meet the requirements above, acceptable verifications will be required to be attached in the Miscellaneous Payee profile in Workday. Acceptable verification can be performed by one of the following methods:

Document Details Phone call (between payee and department) using a previously established/independently sourced phone number Upload a call log document that includes that date, time, phone number, and the name of the person they contacted Official bank document - voided check Check must state "VOID" and contain account details including name, address, and bank account Official bank document - signed bank letter Letter must contain the bank's letterhead confirming account details including name, address, and bank account number Redacted bank statement or online bank screen print Screen print must contain account details including name, address, and bank account number Frequently Asked Questions

Q: Are approvers expected to review both MPE and MPs before approval?

A: Yes, approved must review both MPE and MPs if the ACH transaction is $5,000 or greater AND either of the following conditions applies:

The payee is a new payee, OR

The payee is an existing payee and their banking information is being updated

If both the transaction threshold and one of the conditions mentioned above are met, review of both the MPE and MP is required prior to approval.

Q: Is DocuSign an acceptable form of verification?

A: Yes, but only if the bank information provided is supported with additional verification. Because DocuSign requests remain vulnerable to business email compromise (BEC) and rely on the same communication channel as the original request, additional independent verification is required. This may include the official bank documentation included in the DocuSign file or a callback to the payee using contact information already on file.

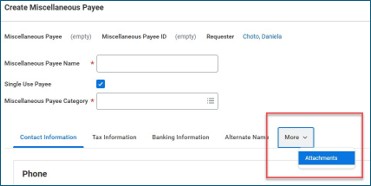

Q: Where do I attach the verification?

A: Include the verification document in the “Attachments” tab of the Miscellaneous Payee. When creating or editing a miscellaneous payee, choose "More", followed by "Attachments"

Q: How should recurring payments be handled?

A: For recurring payments, no additional verification is needed as long as the banking information remains unchanged. If there are any changes to the banking information, and the $5,000 threshold is met, updated verification must be obtained.

Q: Are there any privacy concerns to attaching bank information in the payee profile in Workday?

A: Workday has dual factor authentication and is tokenized. Per NACHA's Supplementing Data Security Requirements, encryption, truncation, tokenization, destruction, or having the financial institution store, host, or tokenize the account numbers, are among options for Originators and Third-Parties to consider.

Q: Are other ACH Payments such as Supplier and Expense Payments affected?

A: Supplier payments are also affected. However, supplier ACH payments are originated through the third-party payment platform Paymode. Paymode already performs account verification on behalf of the University of Washington; therefore, these transactions are currently out of scope for the new ACH Policy.

Expense payments, such as employee reimbursements, are also affected. However, because the banking information is generated through Workday HRP, a separate process must be developed. BAO and Payroll are working together to establish this process, which will be implemented at a later date.

- Miscellaneous Payee Best Practices

- When entering a Miscellaneous Payee in Workday, please make sure the Miscellaneous Payee Category is either:

- Domestic Payee (a non-UW student, non-UW employee who is a U.S. Citizen or Resident Alien)

- Foreign National Payee (a non-UW student, non-UW employee who is a Non-Resident Alien)

- Student (a UW student who is a U.S. Citizen or Resident Alien)

- Student-Foreign (a UW student who is a Non-Resident Alien)

- If the spend category used requires a Social Security Number (SSN), please make sure that only 9 digits are entered.

- The payee's SSN is only required if the spend category is 1099 reportable and the payee will receive $1,500 or more of reportable income in the calendar year.

- Please do not enter any spaces or dashes in the SSN.

- If the payee does not have an SSN or an SSN is not required, please enter 9 zeros in the SSN field.

- Please do not include any special characters (i.e.: period, comma) in the payee's name when entering their information.

- When entering a Miscellaneous Payee in Workday, please make sure the Miscellaneous Payee Category is either:

- Miscellaneous Payments Best Practices

- We recommend only processing payments once the activity has taken place. If you would like to process a payment request in advance, you may only do so up to two weeks before the activity date and the Payment Type must be a check sent through Campus Mail.

- Payment Type:

- Checks:

- To send a check via campus mail, please make sure "Campus Mail" is selected under the Handling Code and please enter the campus box number under Miscellaneous Field 7.

- If the check needs to be picked up at Mailing Services reception desk, use the "Hold-pickup" Handling Code.

- To send a check directly to the payee, please make sure the payee's address is entered under their Contact Information on Workday.

- ACH or Wire:

- "ACH" may only be selected for domestic transactions. If the payee uses a domestic bank (i.e. bank is in the United States), we recommend using the "ACH" payment type.

- If the payee uses a foreign bank (i.e. bank is located outside of the United States), please select the "Wire" Payment Type. All foreign transactions must be completed as a wire.

- Checks:

- If an individual already has an active vendor number, use Supplier Invoice Request to make the payment.

- If a service invoice is over the Direct Buy Limit, do not split the invoice into two different payments.

- Other Considerations

If a check payment for an MP needs to be canceled:

Please visit the Check Cancelation page for guidance.

If the payment is $10,000 or more:

Miscellaneous Payments are not processed for service payments over the Direct Buy Limit of 10K. If a payment is over the Direct Buy Limit, please register the individual as a supplier and submit as a requisition.

If the payee is a foreign national:

- Please refer to the checklists on the Global Operations site for required documents for foreign payments.

- Please upload all required documents to the Docusign Portal.

1099 Misc Tax Reporting Process:

Form 1099-NEC and Form 1099-MISC are issued by the University of Washington at year-end to payees whose total payments meet the IRS reporting threshold. If you have any questions about 1099 reporting please email the 1099 Desk at ten99@uw.edu.

- Please refer to the checklists on the Global Operations site for required documents for foreign payments.