The policy will be implemented only through the Expense Report module, affecting employees and student employees. Students, candidates, and visitors reimbursed through the Miscellaneous Payment module are not affected at this time.

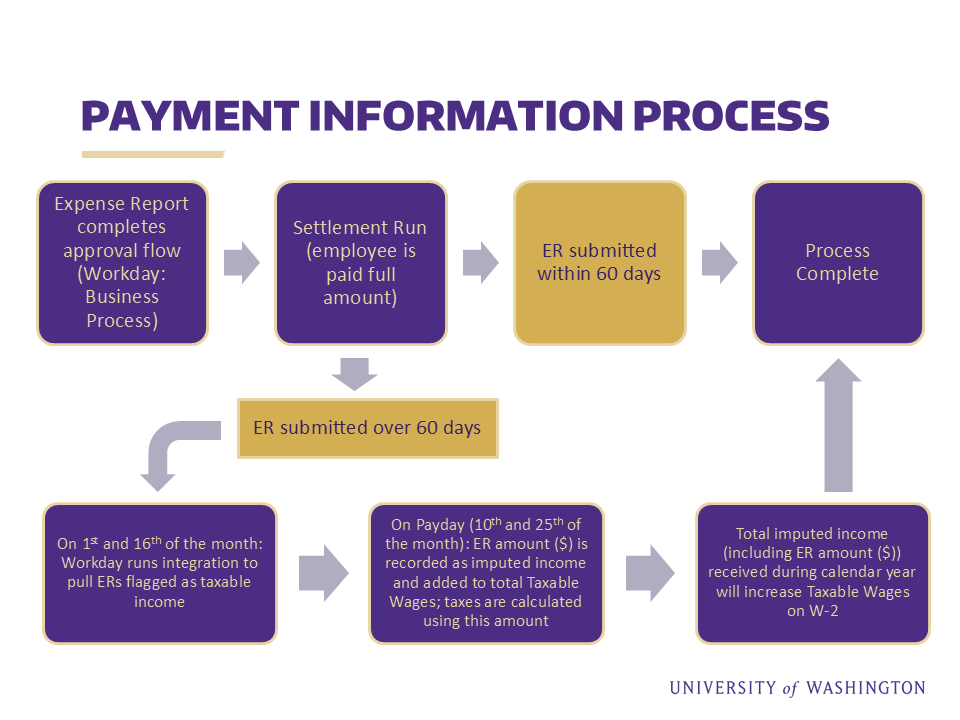

Effective July 06, 2026, UW will adopt Rule 2 of the IRS Accountable Plan (Also referenced in SAAM 10.80.70.b). Under this policy, expenses must be substantiated within 60 days. For purposes of this policy, as stated in the Safe Harbor established in IRS Section 1.62-2(g)(2)(i), 60 days is defined as a "reasonable period of time". Failure to do so will result in the expense being treated as taxable income, and the reimbursement will be processed through payroll to ensure the applicable payroll withholding taxes are applied from the individual's next semi-monthly earnings (see Payment Information Process).

{kind=link}

- From the date the trip ends1 for travel expenses

- From the date of purchase for non-travel expenses

Expenses substantiated on an expense report within this time period will satisfy the reasonable time period requirement and will not be considered income.

Exception documentation must be attached to the delayed expense report.

Allowable exceptions to this policy include:

- The employee was on an approved extended leave of absence.

- Documentation requirement: Department confirmation of extended leave of absence

- The employee was on business travel status for over 60 days.

- Documentation requirement: Trip pre-approval, documentation substantiating continuous 60-day travel

- The delayed submission of the expense report was caused by the Shared Environment and/or department personnel other than the Payee.

- Documentation requirement: SE Director (or SE highest reporting authority) explanation and approval

1Date the trip ends: Last day of the trip, including personal time

Additional Resources:

- June 2026 - Procurement Information Meeting - 60 Day Reimbursement Policy

- YouTube recording, Slide deck, Q&A

- Job Aid - How to Create Travel and Non-Travel Spend Authorizations and Expense Reports: 60 Day Reimbursement Guide

- Updates: Personal Time Questionnaire responses (Page 12), 60 Day Reimbursement (Page 34)

- Payment Information Process (flow chart)